We have seen how the competitive pressures created by accelerating demand tempos lead organizations to develop the requisite agility needed to work with the top-Λ of the double-V cycle – to develop the capabilities for dynamic alignment and synchronization of effects within the client’s context-of-use. These capabilities are necessary to competing in the Q-sectors – the quaternary and quinary sectors of the economy.

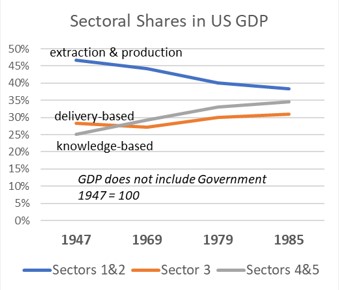

When we think of Volkswagen’s avoidance of the constraints imposed by emissions standards (Naughton 2015), or of the design shortcuts that Boeing made to get the 737 Max to market (Travis 2019), we think of organizations that choose their own interests over those of their customers. These are businesses in the industry sector focused on production processes, referred to as being in the secondary sector[1], which have added a tertiary sector focus on delivery to their end-users using digital technology to enhance the underlying products. The secondary sector’s focus is on capturing supply-side value defined by the direct effects of using its products, for example in these cases being more economical or cheaper to operate. The secondary sector’s share of US GDP (along with the primary sector of extraction industries) has been declining steadily since World War II (see below Sectoral Shares in US GDP 1947-1985 (Kenessey 1987)).

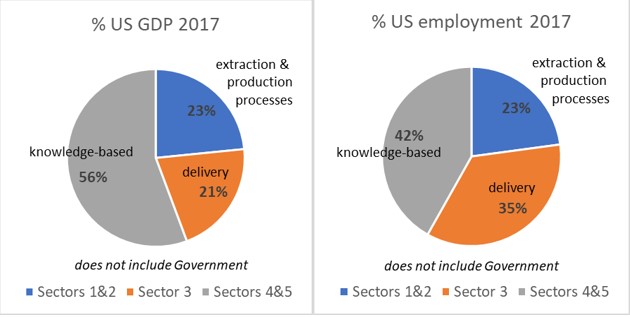

Meanwhile, the share of US GDP taken by the knowledge-based sectors has increased (see above). Knowledge-based organisations in these sectors, for example providing finance and insurance information-based services in the quaternary sector and healthcare cohesion-based services in the quinary sector[2], capture value from the way they diagnose, recommend and respond to client demands that are particular to the client’s singular situation. The value captured in these sectors is from creating demand-side value defined primarily in terms of the indirect effects on clients’ situations, for example by making savings grow faster, ensuring more effective recovery from accidents or offering better treatment of illnesses. This trend towards organisations in the knowledge-based sectors taking an increasing share of GDP continues, in 2017 accounting for nearly 60% of GDP and about 40% of employment (See below Comparisons of US Sector size in 2017 by GDP and employment (Jolliff and Nicholson 2019)).

Note that whereas in the primary extraction and secondary production sectors, % GDP and % employment are comparable (23:23), in the tertiary delivery sector the ratio of employment to GDP is higher (35:21) while in the knowledge-based sectors it is lower (42:56). The relationships between these sectors is summarised below:

One of the effects of this trend is to change the nature of employment opportunities. Another is to change the nature of GDP growth itself and how questions of welfare are approached (Hulten and Nakamura 2019). Instead of growth being defined solely in terms of the sales value of outputs of products and services, it becomes defined also in terms of increasing the use-value of those products and services in both B2B and B2C contexts-of-use (Hulten and Nakamura 2018).

The doctrines of competitive advantage dominant through the latter part of the last century may, best exemplified by Michael Porter’s work (Porter 1985), have endorsed behaviours that put suppliers’ interests above those of customers in pursuit of competitors’ ‘survival of the fittest’. Such behaviours in pursuit of capturing supply-side value reward innovation in the extraction, production and delivery sectors. In the knowledge-based sectors, however, given the nature of the demand-side value being created, clients expect their advisers and doctors to put their interests first. This is something that citizens expect government to secure for them in the long term (Vibert 2014) since, in these sectors, behaviours that put the supplier’s short-term interests first end up being destructive of the social environments in which their clients are to be found, for example by only providing banking services to the already-well-off, leaving many without the benefit of such services (Porter and Kramer 2011), or by the over-use of treatments to maximise utilisation of a healthcare clinic (Committee on Quality of Health Care in America 2001).

And yet we do not typically expect our interests as customers or clients to be put first, unless we are very rich of course and/or tip very well! Nor does it appear to be what citizens believe is happening at the national level, judging by the populist movements in the economies of the West (Brubaker 2017). Perhaps the clearest evidence of this comes from the demonstrations by children challenging politicians’ collective failure to rein in the environmental excesses of industry in the face of a growing pace in climate change (Corner 2019).

What might it be about demand-side value, then, that would lead organisations to approach it not by choosing the interests of one side over the other, but rather by holding both sides as effectively as possible (Boxer 2019). Asymmetric leadership is a way of referring to this ability to hold both sides, an approach to leadership in which the work of the organisation is a work of continuous innovation in the face of the double challenge presented in capturing demand-side value. While perhaps perceived as a luxury for organisations competing in the primary and secondary sectors of extraction and production, asymmetric leadership becomes a necessity in the knowledge-based sectors delivering alignment and cohesion within clients’ contexts-of-use.

References

Boxer, P.J. 2019. ‘Challenging impossibilities: using the plus-one process to explore leadership dilemmas’, Organizational and Social Dynamics, 19: 81-102.

Brubaker, Rogers. 2017. ‘Why Populism?’, Theory and Society, 46: 357-85.

Committee on Quality of Health Care in America. 2001. Crossing the Quality Chasm: A New Health System for the 21st Century (National Academy Press).

Corner, Adam. 2019. ‘The power of the global school strike movement – breaking the ‘us and them’ distinction around climate activism’, Climate Outreach.

Hulten, Charles R., and Leonard I. Nakamura. 2018. “Accounting for Growth in the Age of the Internet: The Importance of Output-Saving Technical Change.” In. https://doi.org/10.21799/frbp.wp.2017.24: Federal Reserve Bank of Philadelphia Research.

———. 2019. “EXPANDED GDP FOR WELFARE MEASUREMENT IN THE 21ST CENTURY.” In. http://www.nber.org/papers/w26578: NATIONAL BUREAU OF ECONOMIC RESEARCH.

Illich, I. 1981. Shadow Work (Marion Boyars: New York).

Jolliff, Billy, and Jessica R. Nicholson. 2019. “Report: An Update Incorporating Data from the 2018 Comprehensive Update of the Industry Economic Accounts.” In, edited by Bureau of Economic Analysis. https://www.bea.gov/media/5481: US Department of Commerce.

Kenessey, Zoltan. 1987. ‘The Primary, Secondary, Tertiary and Quaternary Sectors of the Economy’, The Review of Income and Wealth, 33: 359-85.

Kuzmin, O., O. Pyrog, and L. Melnik. 2014. ‘Transformation of Development Model of National Economies at Conditions of Postindustrial Society’, Econtechmod – An International Quarterly Journal, 3: 41-45.

Naughton, J. 2015. ‘VW’s ‘neat hack’ exposes danger of corporate software’, The Guardian.

Porter, M. E. 1985. Competitive Advantage: Creating and Sustaining Superior Performance (Free Press: New York).

Porter, M. E., and M.R. Kramer. 2011. ‘Creating Shared Value: How to reinvent capitalism – and unleash a wave of innovation and growth’, Harvard Business Review: 2-17.

Travis, Gregory. 2019. “How the Boeing 737 Max Disaster Looks to a Software Developer.” In IEEE Spectrum. https://spectrum.ieee.org/aerospace/aviation/how-the-boeing-737-max-disaster-looks-to-a-software-developer.

Vibert, Frank. 2014. The New Regulatory Space: Reframing Democratic Governance (Edward Elgar: Elgaronline).

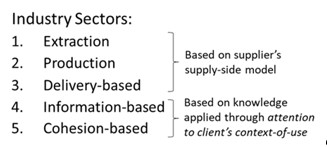

[1] There is still not a widely shared definition of all five sectors, given the dependence of the quaternary and quinary sectors on postindustrial society (Kuzmin, Pyrog, and Melnik 2014) The industries included here in each sector are:

- S1 (extraction): agriculture, forestry and fisheries; mining industry and the development of mining;

- S2 (production processes): manufacturing industry; supply of electricity, gas, steam and conditioned air; water supply, sewerage and waste management; construction;

- S3 (delivery-based): transport, warehousing, postal and courier services; wholesale and retail trade, repair of motor vehicles and motorbikes; arrangement of temporary housing and catering;

- S4 (information-based): financial and insurance services; real estate services; administrative and support services; public administration and defense, compulsory social insurance;

- S5 (cohesion-based): information and telecommunications; digital industry; education; professional, scientific and technical activities; healthcare and social assistance; arts, sports, entertainment and recreation.

[2] The quinary sector represents the highest category of decision makers who formulate policy guidelines in Industry, Govt Departments, Science and Technology which have a profound impact on the economy. Some Australian studies also include women and household activities once done by people in their home, which are not normally included in economic activities and national income. These are activities that ensure cohesion of services around the situation of the decision-maker and/or the household. It is associated with shadow work (Illich 1981) because this is the (frequently unpaid) ‘last mile’ of the work needed to make services cohere around the situation of the end-user.